AI, SMEs, and the New Financial Architecture: Why Community Banks Are Too Many to Fail

Farhad Reyazat – PhD in Risk Management

Citation: Reyazat, F. (2025, July 14). AI, SMES, and the New Financial architecture: Why Community Banks are too many to fail. https://www.reyazat.com/2025/07/14/ai-smes-and-the-new-financial-architecture-why-community-banks-are-too-many-to-fail/

As artificial intelligence rapidly transforms the global workforce, the question looming large isn’t just what jobs will be lost, but who will be most affected, and how societies can respond. In this unfolding narrative, small and medium-sized enterprises (SMEs) are not just peripheral actors—they are the frontline defenders of employment, the actual engine of innovation, and increasingly, the stabilizers of economic resilience.

AI and the Disruption of Jobs: A Tectonic Shift Ahead

According to McKinsey, up to 375 million jobs (14% of the global workforce) could be displaced by automation and AI by 2030. The World Economic Forum’s Future of Jobs Report 2023 projects that 44% of current worker skills will be disrupted within five years, and roles such as data entry clerks, customer service representatives, and bookkeeping clerks are expected to decline by over 25% globally.

In developed countries, the middle-skill segment, which has historically driven stable employment, is most vulnerable. Automation is replacing repetitive tasks, while high-end roles evolve and low-end jobs shrink or shift to gig-based formats.

SMEs: The Adaptive Saviors of the Labor Market

While AI poses threats, SMEs present solutions. Globally, SMEs:

- Account for over 90% of all businesses

- Contribute 60–70% of total employment

- Represent 55% of GDP in high-income economies

- Drive 20% of innovation patents in biotechnology and IT

(Source: WEF, OECD, World Bank)

Unlike large corporations that often use AI to replace jobs, SMEs tend to augment human roles, using AI to enhance productivity without mass layoffs. According to the WEF’s “Data Unleashed” (2023) report:

- 73% of SMEs adopting AI tools reported improved employee efficiency, not workforce reduction.

- 61% said AI allowed existing staff to focus on more creative or strategic tasks.

- Only 9% of SMEs using AI reported actual headcount reductions.

Post-AI Economy: Why SMEs Will Matter Even More

- SMEs are agile and human-centric

SMEs can adapt quickly, creating localised, high-trust employment. As AI reshapes jobs, SMEs offer flexibility that large corporations often lack, allowing displaced workers to reskill and reintegrate more smoothly. - They are incubators of reskilled talent

With appropriate support, SMEs can become training grounds for new skills in digital marketing, AI operations, data handling, and services that require soft skills. They have the potential to absorb displaced labor, provided they have access to capital, cloud tech, and training. - They decentralize opportunity

In a post-AI world where large firms concentrate power and profits, SMEs play a vital role in distributing economic growth across geographies, which is essential for maintaining political and social stability. - They are the true AI adoption frontier

While only 15% of SMEs globally have implemented AI solutions, this figure is set to double by 2030. Affordable, SaaS-based AI tools are already democratizing access, enabling even microbusinesses to automate marketing, improve customer service, and make data-informed decisions.

But There’s a Catch: The Barriers SMEs Face

Despite their potential, SMEs are structurally under-supported:

- Only 44% have a formal cybersecurity policy, and

- Less than 50% have robust data privacy practices

(Source: WEF Data Unleashed, 2023)

Moreover, AI literacy is a significant gap:

- In the UK, only 12% of SMEs report having staff trained in AI basics

- 52% say they lack internal capability even to consider AI use

(Source: Tech Nation AI Report, 2024)

Policy & Investment: A Strategic Imperative

To unlock the post-AI potential of SMEs, multi-level support is critical:

1. Digital Infrastructure Support

Subsidised cloud services, cybersecurity frameworks, and AI toolkits tailored for SMEs.

2. Skills & Training Incentives

Public-private partnerships to upskill SME teams in applied AI, digital transformation, and adaptive management.

3. Financial Access

Simplified access to low-interest AI/digital transformation loans, especially for firms in manufacturing, retail, education, and logistics.

4. Smart Regulation

Ensure data governance, AI safety, and procurement frameworks empower SMEs rather than burden them.

Why Supporting SMEs Is Not Just Smart—It’s Necessary

In an era where AI may centralize wealth and hollow out middle-class jobs, SMEs serve as a counterbalance to this trend. They are not relics of a pre-digital past, but the most strategic vehicles for inclusive innovation and employment in a post-AI future. Supporting SMEs today is an investment in economic stability, democratic resilience, and human dignity tomorrow.

The Underrated Powerhouses: How Community Banks Sustain Small Businesses

In the vast financial ecosystem dominated by mega banks and fintechs, it’s easy to overlook the quiet yet critical role played by community banks. These smaller institutions—defined by their local ownership, personalized approach, and deep community ties—have long been instrumental in supporting small and medium-sized enterprises (SMEs). Despite industry consolidation and mounting regulatory challenges, community banks remain a vital financial lifeline for millions of American entrepreneurs.

Recent research from the Federal Reserve Bank of St. Louis and regulatory agencies highlights the unique value proposition of community banks: they lend a higher proportion to small businesses, approve a greater percentage of loan applications, and foster deeper financial relationships than their larger counterparts. And increasingly, central banking leadership—including figures like Michelle Bowman and Ben Bernanke—are recognizing the systemic importance of maintaining a strong, adaptive community banking sector.

Community Banks: Fewer in Number, Strong in Presence

Over the last two decades, the number of community banks in the U.S. has declined by nearly 46%, from 7,620 in 2003 to just 4,129 in 2023. Yet their physical presence remains substantial, with over 27,000 active branches nationwide, rivaling the combined total of the largest 30 U.S. banking institutions.

This paradox of shrinking institutional numbers and sustained local reach highlights a critical truth: while fewer in quantity, community banks continue to fill an indispensable role, especially in rural and underserved regions where big banks often withdraw.

These banks “invest more than just money; they invest in relationships.” This approach cultivates trust and ensures that even the smallest businesses receive the personalized guidance they need.

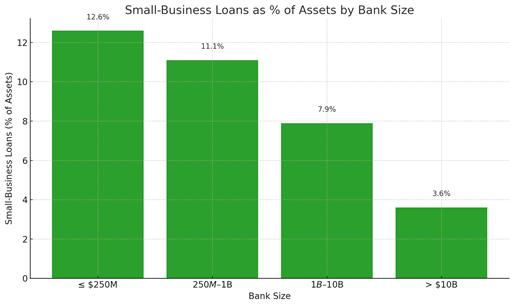

Lending to SMEs: A Disproportionate Commitment

Unlike large banks that diversify into investment banking, asset management, and corporate credit, community banks concentrate on what they do best: serving small businesses.

According to the St. Louis Fed, community banks allocate a significantly higher portion of their portfolios to SME lending:

Their commitment to microloans—under $100,000, often vital for early-stage and solo entrepreneurs—is equally impressive:

- Small community banks: 2.4% of assets

- Mid-sized banks: 1.0%

- Large banks: 0.6%

These numbers demonstrate a mission-aligned model: community banks are not only willing but structurally built to finance SME growth.

Approval Rates and Borrower Experience

Community banks excel not just in intent but in performance. According to the 2022 Small Business Credit Survey:

- 82% of applicants at community banks received at least partial loan approval

- Compared to just 68% at mid- and large-sized banks

- Only 40% of applicants at community banks reported hurdles during the process, versus 50%+ for larger banks and fintechs

Moreover, community banks continue to dominate lending to nonemployer firms, which represent nearly 80% of all U.S. small businesses. In 2022, 58% of sole proprietors secured funding through small banks, compared to 33% at larger institutions.

This higher-touch model isn’t just anecdotal. In his 2011 speech, then-Fed Chair Ben Bernanke noted that during the Great Recession, smaller banks increased small-business lending, even as larger institutions curtailed credit. Their relationships, not just balance sheets, drive lending.

Addressing Equity and Access

Minority Depository Institutions (MDIs)—a specialized category of community banks—play a critical role in addressing the racial and ethnic lending gaps. These institutions serve historically underbanked populations, providing both capital and culturally relevant financial services.

Yet barriers remain: In 2022, only 10% of minority business owners sought loans from small banks, compared to 27% of white entrepreneurs. While this reflects awareness and access gaps, it also signals a tremendous opportunity for MDIs to expand their reach—and for regulators and foundations to support them through targeted capital and capacity-building efforts.

As Michelle Bowman emphasized in her 2024 BIS speech, diversity of institutions—including MDIs and rural banks—is crucial for financial inclusion and systemic resilience.

Pressures and Adaptation in a Changing Landscape

Community banks face increasing pressure to modernize. According to the 2023 CSBS Community Bank Survey:

- Only 40% of community banks currently offer end-to-end digital loan applications

- By contrast, fintechs and large banks offer seamless digital platforms as standard

To remain competitive, many are:

- Partnering with fintechs to update core banking systems

- Outsourcing cybersecurity and compliance functions to third-party vendors

- Adopting real-time payment tools such as the FedNow network

But technology alone won’t ensure sustainability. As the OCC’s Common Sense Approach to Community Banking stresses, strong governance, risk management, and capital planning are equally vital. The OCC encourages boards of directors to align growth strategies with core risks and ensure that innovation does not come at the expense of prudence.

Regulation: Tailored, Not One-Size-Fits-All

In her 2024 address, Governor Michelle Bowman argued that traditional, asset-based regulatory thresholds no longer reflect the evolving nature of community banks. A bank with $1 billion in assets today may operate with greater complexity than a $10 billion institution a decade ago.

She advocates for a risk-sensitive, activity-based approach to supervision, ensuring community banks aren’t burdened by regulations designed for global systemically important institutions (G-SIBs). This echoes Ben Bernanke’s 2011 remarks: “Rules should be proportional and supervision should be risk-focused.”

The OCC echoes this view, urging customized examination scopes, regular dialogue with bank leadership, and hands-on involvement from regulators who understand community bank models.

A Systemic Role in a Local Wrapper

Contrary to the idea that community banks are too small to matter, their collective presence is systemically important.

- They hold a disproportionate share of SME credit

- Dominate lending in rural counties (many of which are single-bank markets)

- Act as local fiscal anchors during crises (e.g., PPP loan distribution)

In sum, they form the “shock absorbers” of America’s economic engine—small in size, but deeply embedded in the financial fabric. As Farhad Reyazat’s research (2015) demonstrates, systemic fragility is not limited to the most prominent players. Using a dynamic factor model applied to EU banks, he shows how even regionally constrained institutions can become conduits of contagion if they are indirectly linked to core nodes in the financial network. In this light, U.S. community banks—despite their modest individual footprints—can collectively exert systemic influence, especially during credit contractions or national shocks. Policymakers must, therefore, evaluate the network role of community banks, not just their standalone metrics. This aligns with Reyazat’s (2015) notion of ‘too-many-to-fail’. Suppose hundreds of community banks simultaneously experience strain due to rising interest rates, real estate downturns, or regulatory burdens. In that case, the cumulative effect can impair credit transmission to millions of small businesses. Thus, safeguarding community banks isn’t just about protecting individual institutions—it’s about preserving the distributed foundation of local credit markets. As Reyazat argues, structural diversity across bank sizes, regions, and business models enhances systemic resilience. Community banks offer differentiated risk appetites and customer relationships that often act countercyclically to those of large banks, especially during crises. Maintaining this diversity should therefore be a deliberate policy objective, not a regulatory afterthought.

Conclusion: To Strengthen the Backbone, Reinvent the Architecture

In a world increasingly shaped by artificial intelligence, automation, and economic uncertainty, small and medium-sized enterprises (SMEs) are not just a sector—they are the foundation of inclusive growth, innovation, and employment. They account for over 90% of businesses worldwide, generate up to 70% of jobs, and serve as the primary engines of opportunity outside concentrated urban tech hubs.

Yet, their future hinges on a critical but underleveraged partner: community banks.

As the data and research show—from the Federal Reserve to the BIS, OCC, and academic findings by Farhad Reyazat in various studies—community banks do more than provide credit. They deliver access, trust, personalization, and resilience. They are disproportionately committed to small business lending, outperform larger institutions in approval rates, and serve as the only financial anchor in thousands of rural and underserved communities.

In the post-AI economy, where digital transformation will displace roles and reorganize industries, SMEs must become adaptive job creators, not just survivors. For this to happen, the financial architecture must shift, placing community banks at the center of economic policy, digital funding, and risk mitigation strategies.

This means:

- Embedding community banks into national AI and digital transition strategies, with priority access to SME digital infrastructure funding.

- Designing tailored regulatory frameworks, as advocated by Michelle Bowman and the OCC, that reflect risk-adjusted proportionality, not institutional size alone.

- Recognizing their network role, as Reyazat argues, in systemic resilience, where the failure of hundreds of small banks can pose as much of a threat as the collapse of a few large ones.

- Using community banks as distribution channels for skilling loans, innovation grants, and real-time payment platforms to underserved and non-digitally native SMEs.

Ultimately, if we want SMEs to continue serving as the real safety net of our economies, we must rebuild the safety net around them. That means financing them not through transactional megabanks or extractive fintechs, but through the very institutions that are relationship-driven, locally trusted, and structurally designed to care about small businesses: community banks.

We don’t need to imagine a more inclusive financial future—we already have the infrastructure in place. We need to elevate it, empower it, and embed it into the heart of our post-AI economic strategy.

The future of work, innovation, and democratic economic participation depends on it.

References

McKinsey Global Institute. (2017). Jobs lost, jobs gained: What the future of work will mean for jobs, skills, and wages. https://www.mckinsey.com/featured-insights/future-of-work/jobs-lost-jobs-gained-what-the-future-of-work-will-mean-for-jobs-skills-and-wages

Organisation for Economic Co-operation and Development (OECD). (2022). SMEs and entrepreneurship. https://www.oecd.org/en/topics/policy-issues/smes-and-entrepreneurship.html

Tech Nation. (2024). AI in UK SMEs: Skills, adoption and barriers (Tech Nation AI Report).

World Bank. (2020). Small and medium enterprises (SMEs) finance. https://www.worldbank.org/en/topic/smefinance

World Economic Forum. (2023). Data unleashed: Empowering small and medium enterprises (SMEs) for innovation and success. https://www3.weforum.org/docs/WEF_Data_Unleashed_Empowering_Small_and_Medium_Enterprises_(SMEs)_for_Innovation_and_Success_2023.pdf

World Economic Forum. (2023). The future of jobs report 2023. https://www.weforum.org/reports/the-future-of-jobs-report-2023

Reyazat, F. (2015). Systemic risk within the global financial architecture: A case study of EU banks (Doctoral dissertation, University of Southampton). ePrints Soton. https://eprints.soton.ac.uk/398053/1/Final%2520PhD%2520thesis%2520-%2520Farhad%2520Reyazat.pdf

Bowman, M. W. (2024, October 2). Building a Community Banking Framework for the Future. Bank for International Settlements. https://www.bis.org/review/r241003a.pdf

Bernanke, B. S. (2011, March 23). Community Banking in a Period of Recovery and Change. Bank for International Settlements. https://www.bis.org/review/r110324c.pdf

Office of the Comptroller of the Currency. (2013). A common sense approach to community banking. https://www.occ.gov/publications-and-resources/publications/banker-education/files/pub-common-sense-approach-to-community-banking.pdf

Western National Bank. (2024, July 24). The heartbeat of local economies: The importance of community banking. https://mywnb.com/news/the-heartbeat-of-local-economies-the-importance-of-community-banking

Federal Reserve Bank of St. Louis. (2023, October). Small banks, big impact: Community banks and small business lending. Regional Economist. https://www.stlouisfed.org/publications/regional-economist/2023/oct/small-banks-big-impact-community-banks-small-business-lending

No Comments